We all know how important credit score is for our ability to take out lending products and qualify for loans or credit cards.

Apart from your credit rating, your debt-to-income ratio is also an essential part of your general financial well-being.

When you know how to calculate your DTI you will be able to define how comfortable you are with your present debt as well as decide if applying for new credit is the wise solution for you at the moment.

In this article, we are going to discuss what a DTI is, how to calculate it, and why it is important to keep it low.

The Basics of Debt-to-Income Ratio

The debt-to-income ratio of the borrower is the percentage of their gross monthly income utilized for debt repayment. Your DTI is calculated by dividing your monthly debt payments by your monthly gross income.

This ratio is used as a percentage. Crediting institutions need to know this figure to understand whether a borrower may afford to pay the loan off and how well he or she manages monthly debt payments.

So, when you say I need 200 dollars now and apply for a new crediting product, the service provider will review if your DTI is high or low.

Borrowers with lower DTI ratios present fewer risks compared to consumers with higher ratios. If your DTI ratio is too high you may have serious monetary issues and trouble paying the debts off on time.

Why DTI Is Important

Some people confuse their debt-to-income ratio with their credit utilization.

While the DTI shows the percentage of the gross monthly income that is used for debt payoff, credit utilization shows the amount of debt a person has to their line of credit and credit card limits.

Many finance-related service providers utilize the DTI of the borrower to understand the loan sum a person may afford based on the amount of their existing debt and present income.

This is especially true about car and mortgage creditors. Different lending products and crediting companies will have different DTI limits.

You may also watch a short but useful video by the Consumer Financial Protection Bureau on what a debt-to-income ratio is and why it matters.

How to Calculate Your DTI Ratio

It isn’t difficult to calculate your debt-to-income ratio. It will give you a better understanding of how much you allocate toward debt repayment every month.

1. Add Up Your Monthly Debts

The first thing you need to do is to total your monthly debts. If you divide your gross monthly income by your monthly debt payments, you will get your DTI ratio.

So, how much total debt do you have every month?

You need to add up all your debt obligations including auto loans, rent or mortgage, minimum credit card payments, student loans, lines of credit, as well as child support/alimony payments.

Health and auto insurance costs and food expenses shouldn’t be added up as these payments aren’t shown on your credit report and don’t impact your rating.

2. Add Up Your Monthly Income

The second step is to calculate how much total monthly income you get. Add up the sum you get from your self-employment or gross income from a W-2 job, alimony/child support, overtime, or bonuses, as well as additional streams of income.

3. Calculate Your DTI Ratio

Now that you know how much exactly you earn and spend on debt payoff every month, you have all the necessary information to calculate your debt-to-income ratio.

To do this, you should divide your monthly debt obligations by your total monthly income. Multiply the final figure by 100 to get a percentage.

What Factors Comprise a DTI Ratio?

Are you planning to take out a mortgage and become a homeowner?

Then you need to know about two components of your debt-to-income ratio that play an important role during application.

It is necessary to admit that there exist two factors mortgage providers utilize for a DTI ratio. This ratio comprises a front-end ratio and a back-end ratio.

Consider the following information to calculate both of them:

- The front-end ratio is often called a housing ratio. This figure demonstrates a percentage of monthly gross income that would be used for housing costs, including property taxes, mortgage payments, homeowners association charges as well as homeowners insurance.

- Back-end ratio. It demonstrates the percentage of monthly income necessary to cover all the monthly debt payments together with housing costs and mortgage obligations. This type of ratio comprises child support, credit card payments, student loans, auto loans, and other types of debt that appear on the credit report.

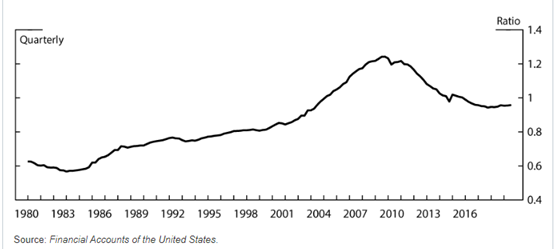

The following figure demonstrates the aggregate nationwide DTI for the USA, as reported by the Federal Reserve. This figure shows a connection between economic growth during the Great Recession and household leverage.

As we can see, aggregate DTI had been slowly rising since the 1980s and experienced a sudden housing boom in the 2000s. After that, it started decreasing during the financial downturn in 2008.

Is There a Perfect Debt-to-Income Ratio?

When you are willing to take out a personal loan, a new credit card, or apply for a mortgage, you need to know if your current DTI ratio is in good standing.

Crediting companies want to see a perfect front-end ratio that is up to 28 percent, while the back-end ratio needs to be up to 36 percent.

Of course, the lenders will take into consideration various factors during your application.

Depending on the lending tool you apply for, your assets, savings, as well as credit rating, the crediting institution may even accept a higher DTI ratio.

Many traditional banking institutions accept a higher ratio of up to 50 percent.

Concluding thoughts…

Summing up, your DTI ratio is used to show how likely you are to make your loan payments regularly as a borrower. This percentage is really important during the application for a new crediting tool or a mortgage.

A lower figure proves that you can manage your finances and won’t have trouble with debt payoff.

This percentage doesn’t impact the credit rating of the borrower but many lenders review it during the loan application.

If your current DTI ratio is too high, you may want to create a budget to track your monthly spending and avoid taking on additional debt.