We’ve all encountered unexpected bills, and they can be incredibly stressful. According to a 2023 report, roughly 1 in 5 Americans gets surprised with a confusing medical bill, even from an in-network provider. I know that anxious feeling.

Take a deep breath; there are ways to handle these situations calmly and without panicking.

In this article, I want to walk through some practical, step-by-step tips on what to do when a bill comes out of nowhere. In this article, you will discover unique strategies to help you manage unexpected bills.

Assessing the Situation

When you get unexpected bills, it’s crucial for you to fully assess the situation before jumping into problem-solving mode. Getting a complete picture of where the surprise expenses are coming from and how urgent the bills are will inform the priority-setting and decision-making processes.

Take Inventory of All Outstanding Bills

- Gather recent statements from all your accounts to understand total owed amounts across mortgages, credit cards, medical providers, home equity loans, auto financing, student loans, personal loans, retail credit cards, utility companies, insurance policies, cell phone/internet bills, subscription services, and any other recurring payments.

- For irregular expenses such as medical bills or home repairs, gather all invoices, estimates, and communications from service providers that outline what you owe.

- Organize these materials so you can see the comprehensive list of financial obligations you are facing, both regular and unexpected.

Evaluate the Degree of Urgency

With all outstanding bills gathered in one place, evaluate each obligation based on its severity and how quickly action needs to be taken.

- Most Urgent: Bills tied to essential utilities like electricity, water, and gas that could face shut-offs if unpaid. Also includes essential costs like groceries, transportation to work, rent/mortgage, insurance premiums, and medications. You can get prequalified for a personal loan in these times of emergency, which could save you from getting stuck in irrecoverable debt.

- Moderately Urgent: Bills with upcoming due dates that would result in late fees or other penalties if missed. Examples include student loan payments, car loans, alimony or child support, minimum credit card payments, and cell phone bills.

- Less Urgent: Revolving credit card balances without immediate due dates for the full amount owed and other debts like personal loans with reasonable minimum payments that could be temporarily reduced while managing higher priority obligations.

Gaining an accurate understanding of the due dates, late penalties, interest charges, and other implications across all outstanding bills allows for smarter prioritization of payments.

Prioritizing Payments

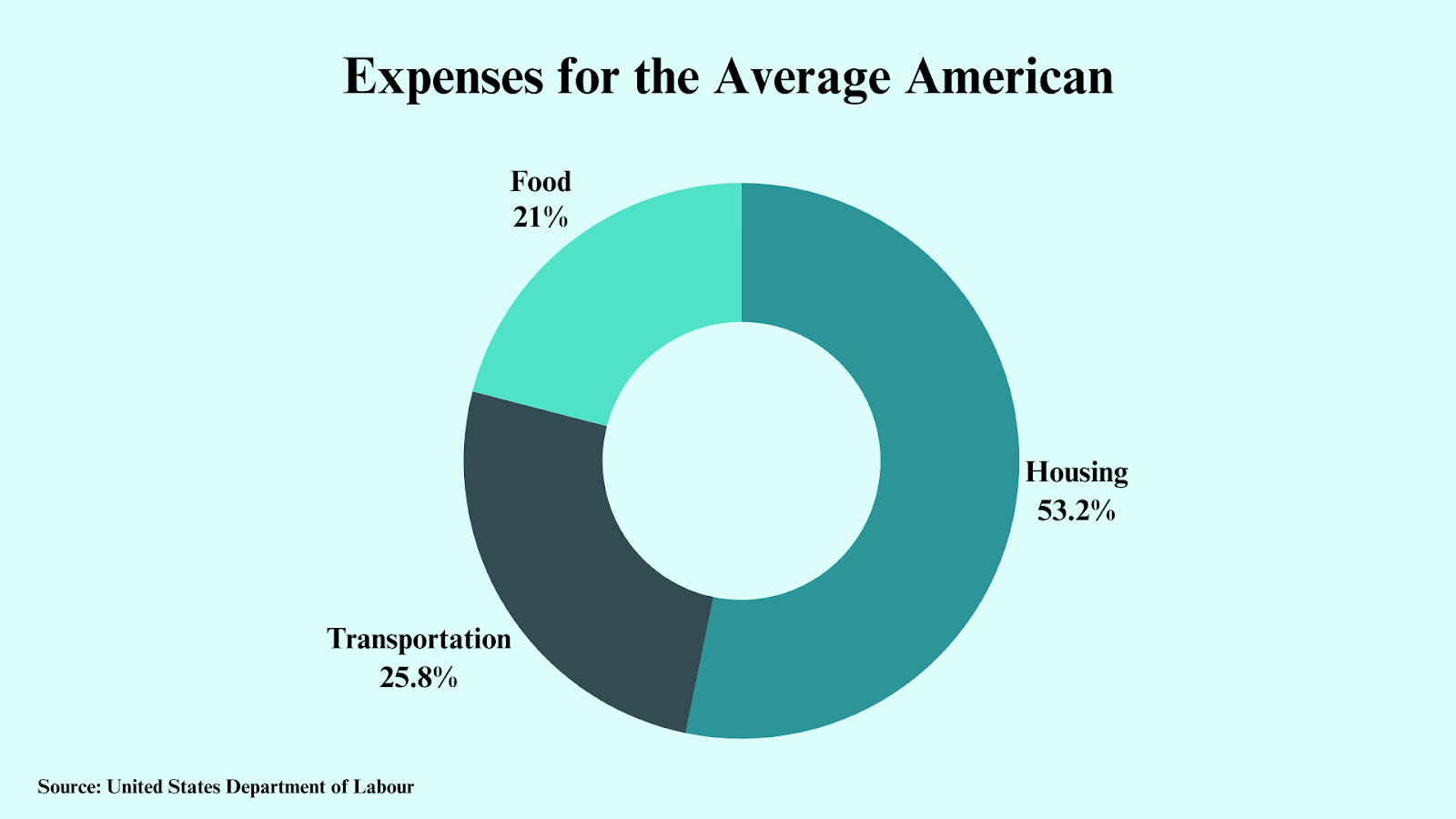

With your obligations categorized by urgency, it’s time to prioritize making payments. Look at the data below that shows the average percentage of expenses for average Americans:

As you strategize bill payments, keep in mind that not all expenses are equal. Housing, transportation, and food costs make up over 60% of the average American’s annual expenditures, according to the Bureau of Labor Statistics. Paying for necessities should take precedence.

Additionally, debts like credit cards carry high interest rates – the average is around 15.7%, according to CreditCards.com. Get in touch with your creditors to explain your situation and try to negotiate lower rates. The Consumer Financial Protection Bureau found that 49% of consumers who contacted their credit card company about financial hardship were able to get more favorable terms.

If negotiation fails, establishing payment plans can be a last resort to keep accounts from going into default as you tackle higher-priority emergency expenses.

Creating a Budget and Emergency Fund

In tandem with addressing these unexpected new bills, it’s important to implement financial best practices moving forward so you have an adequate buffer for life’s curveballs.

Track Expenses

- Utilize a free budget template or budgeting app to capture day-to-day spending across necessities, variable expenses like food and gas, and discretionary purchases for at least one month.

- Categorize transactions to see where your money is going and quickly identify areas of excess that could be reduced.

- Analyze averages across categories to create a reasonable baseline monthly budget aligned with your income and financial goals.

Trim Discretionary Costs

- With better visibility from detailed tracking, identify discretionary expenses that could be cut back without major lifestyle impacts, such as dining out, subscription services, ride shares, brand name groceries, salon visits, and more. Evaluate needs vs. wants.

- Set limits on spending in non-essential categories to free up cash that could be contributed to an emergency fund. Auto-transfer those savings each month so they remain protected from unexpected bills rather than getting folded into discretionary budgets.

Build Emergency Savings

- Having 3-6 months’ worth of living expenses available in emergency savings vastly reduces stress and risk when faced with unplanned bills.

- Contribute regularly each month to a high-yield savings account; even small amounts add up over time. Set up automatic transfers from each paycheck.

- Dip into your emergency savings only for genuine financial emergencies, such as job loss, hospitalization, or home repairs, rather than frivolous expenses that can deplete your fund.

With diligent tracking, cost-cutting, and automated saving, you can build long-term resilience against surprise expenses that throw budgets off track.

Seeking Financial Assistance

For those truly struggling, it can be wise to swallow your pride and seek aid to avoid accounts going into collections or critical services like utilities being shut off for non-payment.

Federal, state, and local government agencies administer assistance programs helping households pay for basics like food, housing, utilities, medical care, and more. Reach out to confirm your eligibility and application requirements.

Additionally, charities and non-profit organizations provide urgent financial relief across causes like hunger, affordable housing, medical bills, disaster recovery, education, employment, and much more. Consult reputable databases to find local non-profits aligned with your needs.

While seeking aid takes some humility, utilize any resources to avoid further financial consequences from unexpected obligations going unpaid.

Avoiding Future Unexpected Bills

Tips for Avoiding Unexpected Bills in the Future – You can take steps now to reduce the chances of unexpected bills later. Doing a little work now saves you big problems down the road.

1. Get Good Insurance

Having insurance helps when bad things happen.

- Health insurance – Covers doctor and hospital costs when you get sick or hurt. Check it every year to make sure it works for you.

- Home or renter’s insurance – Covers your belongings in case of events like theft or damage.

2. Do Regular Maintenance

Fixing little stuff stops big stuff from breaking later.

- Furnace – Have it checked before winter comes.

- AC and heating system – Service them twice a year.

- Roof and chimney – Check every year.

- Smoke detectors – Push the test button monthly.

3. Building an Emergency Fund

- Set aside a portion of your income each month as an emergency fund for unexpected expenses.

- Try not to use this emergency money except for big, important things like losing a job, health problems, or home issues.

Nobody enjoys surprise bills, but you can regain control by planning. This way, you’ll worry less when unexpected expenses do arise.

Frequently Asked Questions

1. What should I do if I can’t pay all my bills at once?

Prioritize paying essential living expenses first while negotiating with creditors on your other accounts. Explain your situation and try to reach new payment agreements appropriate to your budget.

2. Are there government programs that can help with unexpected medical bills?

Yes. Medicaid, Medicare, the Children’s Health Insurance Program (CHIP), and ACA Marketplace plans administer assistance in paying expensive medical bills for those eligible. Reach out to confirm your qualifications.

3. How can I negotiate with creditors for lower interest rates?

Contact creditors directly, explain your financial hardship, provide evidence if possible, and request lower rates or modified repayment terms better suited to your budget. Come prepared with a specific proposal tailored to your situation.